Historiquement l’obligation de facturation électronique a été introduite pour la sphère publique en 2017 avec le portail “Chorus Pro”, puis elle a été progressivement étendue à ses fournisseurs jusqu’en 2020(Flux B2G). Dans les prochaines années, l’obligation de facturation électronique va progressivement s’étendre aux transactions entre entreprises (Flux B2B) avec le nouveau portail “PPF”.

Les deux portails “Chorus-Pro” et “PPF” sont développés par l’AIFE (Agence pour l’informatique financière de l’Etat) ils sont mis à jour très régulièrement, intégrant continuellement de nouvelles fonctionnalités. Ils sont accessibles à titre gratuit en mode manuel, mais ils peuvent aussi être utilisés en mode EDI et API pour automatiser les échanges.

B2B electronic invoicing

The regulatory framework for the extension of electronic invoicing to business-to-business (B2B) transactions is now known.

Decree no. 2022-1299 of October 7, 2022 and articles 289-bis, 290 and 290-A of the General Tax Code set out the rules for electronic invoicing (e-invoicing) and the transmission of invoicing and payment data (e-reporting). These provisions will apply to all VAT-registered businesses in France.

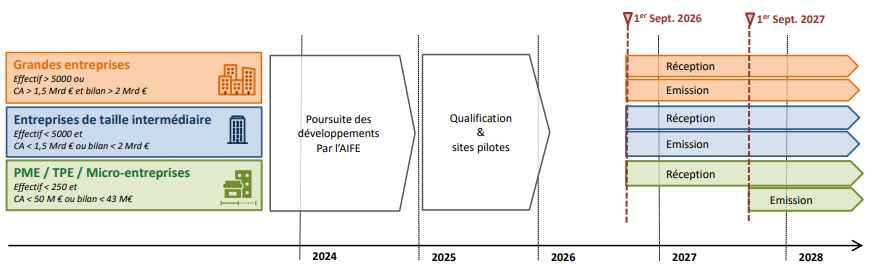

The entry into force of these measures has been postponed by amendment n°I-5395 tabled on October 17, 2023 as part of the Finance Bill for 2024.

The new timetable provides for :

- For large and medium-sized companies, full entry into force on September 1, 2026.

- For all other companies (SMEs/PSEs/Micro-enterprises) a phased introduction

- The obligation to take delivery by September 1, 2026 .

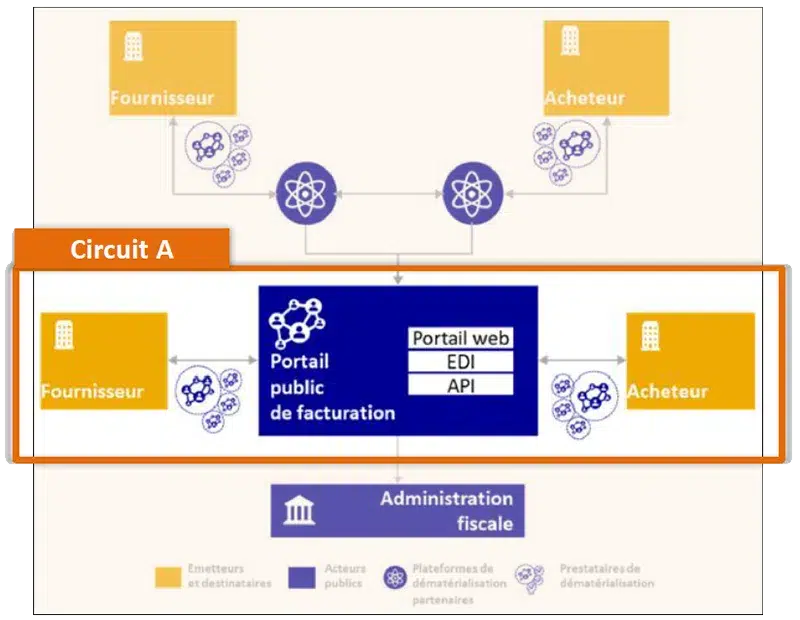

Circuit A of the ” en Y ” diagram

In the external specifications for B2B electronic invoicing published by the AIFE, the various players appear in the ‘Y schema’ derived from article 289 bis of the CGI. In this diagram, the direct connection to the PPF used by A2C is referenced as ‘Circuit A’ between two actors who use the public invoicing portal directly.

The advantages of a direct connection are :

- Lower costs, as PPF’s API services are free of charge,

- Simplicity, as direct communication to PPF eliminates the need for third parties (OD or PDP),

- Compliance, as invoices are issued directly by A2C in the standard UBL format expected by the PPF.

- Robustness, because this implementation choice allows us to control the flow and avoid the hazards associated with the multiplication of players and interfaces.

The A2C connector covers both functional perimeters of the A circuit, using dedicated APIs:

- The issue flow for the ” Supplier ” role, which includes e-invoicing and e-reporting of customer invoices issued.

- The incoming flow for the ” Buyer ” role, which includes e-invoicing and e-reporting of incoming supplier invoices.

Frequently asked questions : Applium has the answers!

Who’s concerned?

The reform applies to all companies established in France and subject to VAT, whether or not they are liable for VAT. However, there are certain exceptions, such as taxable persons who carry out exclusively exempt operations as defined in articles 261 to 261 E of the CGI (health, education, etc.).

What is the impact on invoicing for my French and foreign customers?

The reform contains two complementary obligations:

- e-invoicing, if your business partner is also subject to VAT and established in France,

- e-reporting, the obligation to transmit transaction data (e-reporting) if your business partner is a foreign company or an individual customer.

Does this reform mean the end of the ” paper ” invoice?

- Yes, for exchanges between French companies, paper invoicing is prohibited.

- No, for exchanges with foreign companies or end customers.

Paper” invoicing is prohibited when the issuer and recipient of the invoice are subject to VAT and established in France. Direct transfer of the invoice between sender and recipient is also prohibited.